What is economic indicator backtesting? How does it help?

Problem: Financial analysts and economists need to forecast key economic indicators like CPI, unemployment, and market indices. Univariate models can miss important relationships between economic variables, leading to less accurate predictions. Further, analysts need a way to perform what-if scenario analysis by testing different assumptions about future economic conditions. Our approach: We show how to use Synthefy’s multi-variate forecasting API to leverage relationships between economic indicators (GDP, Federal Funds Rate, Unemployment, CPI, S&P 500) to improve forecast accuracy through backtesting on historical data. We demonstrate three scenarios: univariate baseline, multivariate with macroeconomic indicators, and multivariate with “leaked” indicators (known future values) to enable powerful what-if forecasting. Outcome: Multi-variate models show significant improvement over univariate forecasts, and we show that Synthefy’s what-if forecasting is even more powerful, showing further improvements over the baseline univariate forecasting.1. Setup and Data Loading

This example demonstrates forecasting CPI (Consumer Price Index) using macroeconomic indicators from FRED and Haver APIs. First, let’s set up our imports and API keys:import asyncio

import os

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from fredapi import Fred

from haver import Haver

from sklearn.metrics import (

mean_absolute_error,

mean_absolute_percentage_error,

mean_squared_error,

)

from swarm_visualizer.utility.general_utils import set_plot_properties

from synthefy.api_client import SynthefyAsyncAPIClient

from synthefy.data_models import ForecastV2Request

# Set plot properties

set_plot_properties(usetex=False)

# API Setup

FRED_API_KEY = os.getenv("FRED_API_KEY")

HAVER_API_KEY = os.getenv("HAVER_API_KEY")

SYNTHEFY_API_KEY = os.getenv("SYNTHEFY_API_KEY")

if not FRED_API_KEY or not HAVER_API_KEY or not SYNTHEFY_API_KEY:

raise ValueError(

"FRED_API_KEY, HAVER_API_KEY, and SYNTHEFY_API_KEY must be set"

)

# Forecasting configuration

TARGET_COLUMN = "CPIAUCSL_pct_change"

METADATA_COLUMNS = [

"FEDFUNDS_pct_change",

"GDPH_pct_change",

"UNRATE_pct_change",

"SPY_pct_change",

]

print(f"Forecasting for target column: {TARGET_COLUMN}")

FORECAST_WINDOW = 1 # Forecast 1 quarter ahead

NUM_BACKTEST_ROWS = 12 # Backtest last 12 quarters (3 years)

# Initialize Haver and FRED

haver = Haver(api_key=HAVER_API_KEY)

fred = Fred(api_key=FRED_API_KEY)

# Plot colors

COLORS = {

"univariate": "#2563eb",

"multivariate": "#16a34a",

"multivariate_leak": "#fea333",

"groundtruth": "black",

}

API Keys Required: You’ll need API keys from FRED and Haver Analytics to run this example.

2. Data Collection Functions

Let’s create functions to fetch economic indicators from FRED and Haver:Show data collection code

Show data collection code

def get_haver_series(haver_code, column_name):

"""

Retrieve data from Haver and calculate percent change.

Args:

haver_code: Haver code (e.g., "GDPHA@USECON")

column_name: Name for the value column

Returns:

pd.DataFrame: DataFrame with date, value, and percent change columns

"""

df = haver.read_df(haver_codes=[haver_code])

df = df[df.columns[df.columns.isin(["date", "value"])]]

df = df.dropna()

df = df.rename(columns={"value": column_name})

df["date"] = pd.to_datetime(df["date"])

pct_change_column = f"{column_name}_pct_change"

df[pct_change_column] = df[column_name].pct_change().dropna()

return df

def get_haver_gdp():

"""Retrieve Real GDP from Haver (GDPHA from USECON database)."""

return get_haver_series("GDPHA@USECON", "GDPH")

def get_federal_funds_rate():

"""Retrieve Federal Funds Effective Rate from FRED."""

df = (

fred.get_series("FEDFUNDS", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "FEDFUNDS"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_unemployment_rate():

"""Retrieve Unemployment Rate from FRED."""

df = (

fred.get_series("UNRATE", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "UNRATE"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_consumer_price_index():

"""Retrieve Consumer Price Index from FRED."""

df = (

fred.get_series("CPIAUCSL", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "CPIAUCSL"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_sp500():

"""Retrieve S&P 500 Index from Haver."""

return get_haver_series("SP500@USECON", "SPY")

3. Combine and Aggregate Data

Now let’s combine all economic indicators and aggregate to quarterly frequency:def create_combined_dataset():

"""

Combine economic indicators into a single dataset with percent changes,

aggregated to quarterly frequency.

Returns:

pd.DataFrame: Combined dataset with all indicators as percent changes (1990+), quarterly

"""

# Fetch all data sources

gdp_df = get_haver_gdp()

fed_funds = get_federal_funds_rate()

unemployment = get_unemployment_rate()

cpi = get_consumer_price_index()

sp500 = get_sp500()

# Merge monthly indicators

macro_df = (

fed_funds.merge(unemployment, on="date", how="outer")

.merge(cpi, on="date", how="outer")

.merge(sp500, on="date", how="outer")

)

macro_df["date"] = pd.to_datetime(macro_df["date"])

macro_df = macro_df.set_index("date")

# Join with GDP (yearly) and forward-fill to monthly frequency

gdp_df["date"] = pd.to_datetime(gdp_df["date"])

gdp_indexed = gdp_df.set_index("date")[["GDPH_pct_change"]]

combined_df = gdp_indexed.join(macro_df, how="outer")

combined_df["GDPH_pct_change"] = combined_df["GDPH_pct_change"].ffill()

# Calculate percent changes for monthly indicators

for col in ["FEDFUNDS", "UNRATE", "CPIAUCSL", "SPY"]:

combined_df[f"{col}_pct_change"] = combined_df[col].pct_change()

# Filter to 1990+ and keep only percent change columns

combined_df = combined_df[combined_df.index >= "1990-01-01"]

combined_df = combined_df.filter(like="_pct_change").ffill().dropna()

# Resample to quarterly frequency (taking the mean of each quarter)

combined_df = combined_df.resample("QE").mean()

return combined_df

# Load the data

df = create_combined_dataset()

print(f"Data shape: {df.shape}")

print(f"Date range: {df.index.min()} to {df.index.max()}")

print(df.head().to_markdown())

| date | GDPH_pct_change | SPY_pct_change | FEDFUNDS_pct_change | UNRATE_pct_change | CPIAUCSL_pct_change |

|---|---|---|---|---|---|

| 1990-03-31 00:00:00 | 0.018857 | -0.00186627 | 0.00303472 | -0.0186932 | 0.00430453 |

| 1990-06-30 00:00:00 | 0.018857 | 0.0212617 | 0.000448915 | 0.000474834 | 0.00336038 |

| 1990-09-30 00:00:00 | 0.018857 | -0.0429016 | -0.00357724 | 0.0430479 | 0.00662899 |

| 1990-12-31 00:00:00 | 0.018857 | 0.0143365 | -0.0373292 | 0.0223255 | 0.00426035 |

| 1991-03-31 00:00:00 | -0.00108403 | 0.0435705 | -0.0570111 | 0.0258087 | 0.00148939 |

Quarterly Aggregation: We aggregate monthly data to quarterly frequency using

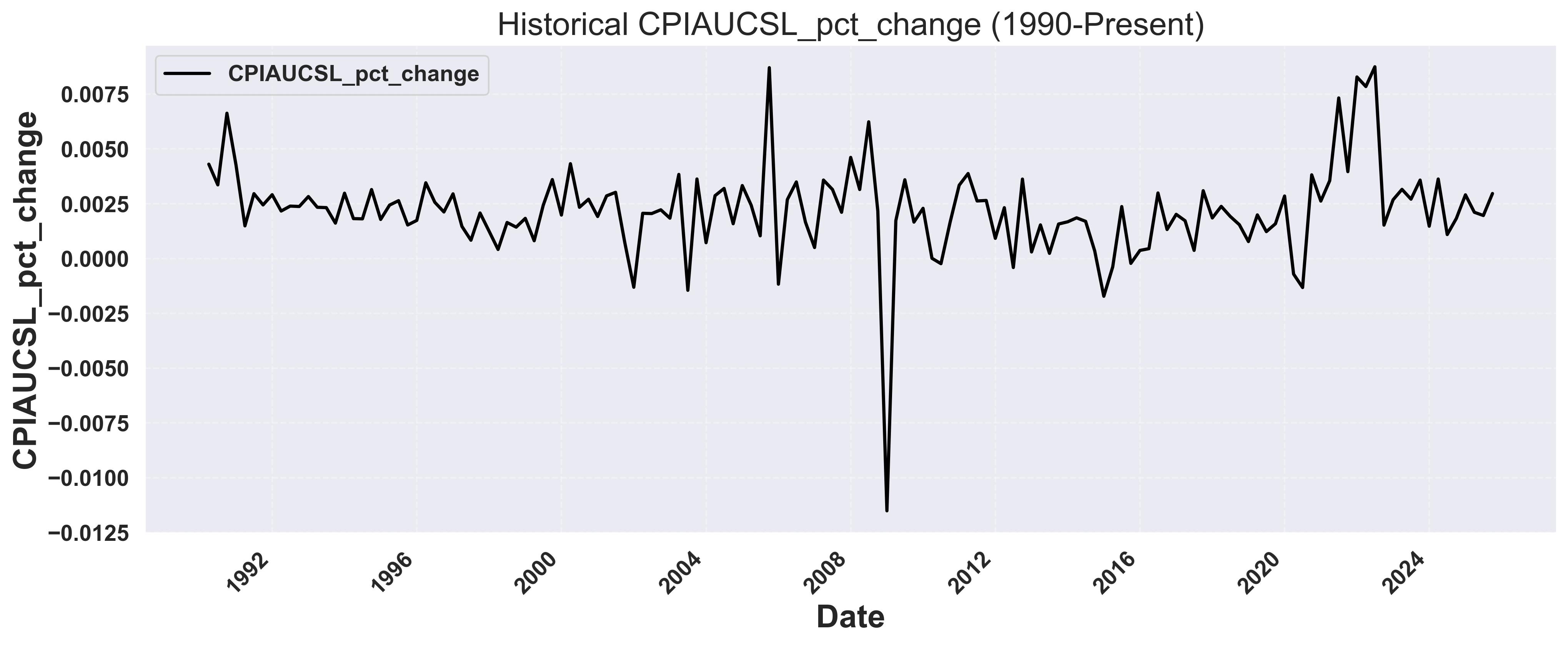

.resample("QE").mean() to align with GDP reporting cycles and reduce noise. Each row represents one quarter with percent changes for all economic indicators.4. Visualize Historical Data

Let’s visualize the historical CPI percent change over time:Show plotting code for raw time series

Show plotting code for raw time series

def plot_raw_time_series(df, output_dir="usecases/economic_backtesting"):

"""

Plot raw time series data for the target variable.

Args:

df: DataFrame with date index and target column

output_dir: Directory to save the plot

"""

os.makedirs(output_dir, exist_ok=True)

fig, ax = plt.subplots(figsize=(14, 6))

# Plot the target column

ax.plot(

df.index,

df["CPIAUCSL_pct_change"],

color="black",

linewidth=2,

label="CPI % Change",

zorder=2,

)

# Set labels and title

ax.set_xlabel("Date")

ax.set_ylabel("CPI % Change")

ax.set_title("Historical CPI Percent Change (1990-Present, Quarterly)")

# Add grid and legend

ax.grid(True, linestyle="--", alpha=0.3)

ax.legend(loc="upper left", frameon=True)

# Format x-axis

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

# Save plot

plot_path = os.path.join(output_dir, "raw_time_series.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Raw time series plot saved to: {plot_path}")

plt.close()

# Plot the raw data

plot_raw_time_series(df)

Example Output: Historical CPI Data

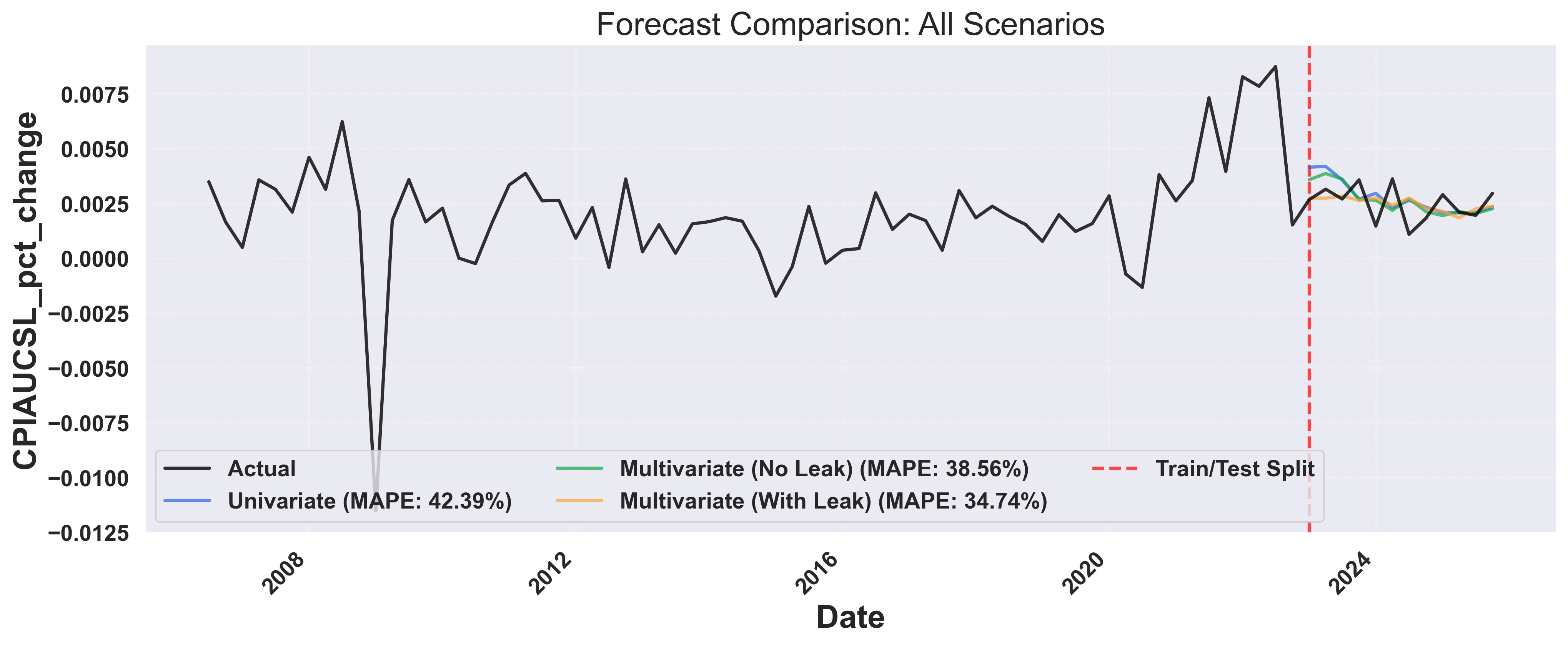

5. Run Backtesting Scenarios

Now let’s run three forecasting scenarios to compare performance:- Univariate: Forecast using only CPI history

- Multivariate (No Leak): Add other economic indicators as context

- Multivariate (With Future Leak): Include future variables (e.g., Fed Funds Rate)

Show backtesting code

Show backtesting code

# Configuration

TARGET_COLUMN = "CPIAUCSL_pct_change"

METADATA_COLUMNS = [

"FEDFUNDS_pct_change",

"GDPH_pct_change",

"UNRATE_pct_change",

"SPY_pct_change",

]

FORECAST_WINDOW = 1 # Forecast 1 quarter ahead

NUM_BACKTEST_ROWS = 12 # Backtest last 12 quarters (3 years)

def calculate_metrics(actual, predicted):

"""Calculate forecast accuracy metrics using scikit-learn."""

mae = mean_absolute_error(actual, predicted)

rmse = np.sqrt(mean_squared_error(actual, predicted))

mape = mean_absolute_percentage_error(actual, predicted) * 100

return {"MAE": mae, "RMSE": rmse, "MAPE": mape}

def extract_actuals_and_predictions(response, request, df_with_date):

"""Extract actual and predicted values from forecast response."""

all_actuals = []

all_predictions = []

for forecast_row, sample in zip(response.forecasts, request.samples):

if forecast_row[0].values:

target_dates = pd.to_datetime(forecast_row[0].timestamps)

predictions = forecast_row[0].values

actuals = []

for date in target_dates:

actual_val = df_with_date[df_with_date["date"] == date][

TARGET_COLUMN

].values

if len(actual_val) > 0:

actuals.append(actual_val[0])

if len(actuals) == len(predictions):

all_actuals.extend(actuals)

all_predictions.extend(predictions)

return all_actuals, all_predictions

async def run_backtest(df, metadata_cols=None, leak_cols=None):

"""

Generic backtesting function for target column forecasting.

Args:

df: Combined economic dataset

metadata_cols: List of metadata columns to use (None for univariate)

leak_cols: List of columns to leak (None for no leak)

Returns:

tuple: (metrics, response)

"""

# Prepare data

if metadata_cols is None:

# Univariate: only target column

data_df = df.reset_index()[["date", TARGET_COLUMN]].copy()

metadata_cols = []

else:

# Multivariate: target column + other indicators

data_df = df.reset_index().copy()

# Create backtesting request

request = ForecastV2Request.from_dfs_pre_split(

dfs=[data_df],

timestamp_col="date",

target_cols=[TARGET_COLUMN],

model="Migas-1.0",

num_target_rows=NUM_BACKTEST_ROWS,

forecast_window=FORECAST_WINDOW,

stride=FORECAST_WINDOW,

metadata_cols=metadata_cols,

leak_cols=leak_cols or [],

)

# Make forecast

async with SynthefyAsyncAPIClient() as client:

response = await client.forecast(request)

# Calculate metrics

all_actuals, all_predictions = extract_actuals_and_predictions(

response, request, data_df

)

metrics = calculate_metrics(all_actuals, all_predictions)

return metrics, response

async def run_all_backtests():

"""Run all three backtesting scenarios and compare results."""

df = create_combined_dataset()

# Run three scenarios in parallel

results = await asyncio.gather(

run_backtest(df, metadata_cols=None, leak_cols=None),

run_backtest(df, metadata_cols=METADATA_COLUMNS, leak_cols=None),

run_backtest(df, metadata_cols=METADATA_COLUMNS, leak_cols=METADATA_COLUMNS),

)

metrics1, response1 = results[0]

metrics2, response2 = results[1]

metrics3, response3 = results[2]

return df, (metrics1, metrics2, metrics3), (response1, response2, response3)

# Run backtests

df, metrics_list, responses = asyncio.run(run_all_backtests())

metrics1, metrics2, metrics3 = metrics_list

6. Compare Results

Let’s print the comparison of all three scenarios:def print_comparison_summary(metrics1, metrics2, metrics3):

"""Print formatted comparison table of all three scenarios."""

print(f"\n{'Scenario':<45} {'MAE':>10} {'RMSE':>10} {'MAPE':>10}")

print("-" * 80)

scenarios = [

("1. Univariate (target only)", metrics1),

("2. Multivariate (No Leak)", metrics2),

("3. Multivariate (With Leak)", metrics3),

]

for name, m in scenarios:

print(

f"{name:<45} {m['MAE']:>10.6f} {m['RMSE']:>10.6f} {m['MAPE']:>9.2f}%"

)

print_comparison_summary(metrics1, metrics2, metrics3)

Scenario MAE RMSE MAPE

--------------------------------------------------------------------------------

1. Univariate (target only) 0.000893 0.001020 42.39%

2. Multivariate (No Leak) 0.000812 0.000941 38.56%

3. Multivariate (With Leak) 0.000671 0.000825 34.74%

7. Visualize Forecast Comparison

Create a comprehensive visualization showing all forecast scenarios:Show forecast comparison plotting code

Show forecast comparison plotting code

def plot_forecast_comparison(df, responses, metrics_list, output_dir="economic_backtesting"):

"""

Plot comparison of all three forecasting scenarios.

Args:

df: Combined economic dataset with date index

responses: Tuple of (response1, response2, response3)

metrics_list: List of (metrics1, metrics2, metrics3)

output_dir: Directory to save the plot

"""

os.makedirs(output_dir, exist_ok=True)

response1, response2, response3 = responses

metrics1, metrics2, metrics3 = metrics_list

# Prepare data

data_df = df.reset_index()[["date", TARGET_COLUMN]].copy()

# Find the earliest forecast date to determine train/test split

earliest_forecast_date = None

for forecast_row in response1.forecasts:

if forecast_row[0].values:

dates = pd.to_datetime(forecast_row[0].timestamps)

if earliest_forecast_date is None or dates.min() < earliest_forecast_date:

earliest_forecast_date = dates.min()

# Calculate cutoff to show last 50% of historical data before forecasts

historical_before_forecast = data_df[data_df["date"] < earliest_forecast_date]

cutoff_idx = int(len(historical_before_forecast) * 0.5) # Show last 50% of history

cutoff_date = historical_before_forecast.iloc[cutoff_idx]["date"]

# Filter to show last 50% of historical data + all forecasts

data_df_filtered = data_df[data_df["date"] >= cutoff_date].copy()

fig, ax = plt.subplots(figsize=(14, 6))

# Plot ground truth (last 50% of history)

ax.plot(

data_df_filtered["date"],

data_df_filtered[TARGET_COLUMN],

color=COLORS["groundtruth"],

linewidth=2,

label="Actual",

zorder=4,

alpha=0.8,

)

# Extract and plot forecasts for each scenario

scenarios = [

(response1, metrics1, "univariate", "Univariate"),

(response2, metrics2, "multivariate", "Multivariate (No Leak)"),

(response3, metrics3, "multivariate_leak", "Multivariate (With Leak)"),

]

for response, metrics, color_key, label in scenarios:

# Collect all forecast points across all windows

all_forecast_dates = []

all_forecast_values = []

for forecast_row in response.forecasts:

if forecast_row[0].values:

dates = pd.to_datetime(forecast_row[0].timestamps)

predictions = forecast_row[0].values

all_forecast_dates.extend(dates)

all_forecast_values.extend(predictions)

# Combine all forecasts into a single DataFrame

if all_forecast_dates:

combined_forecast_df = pd.DataFrame(

{"date": all_forecast_dates, "forecast": all_forecast_values}

)

# Remove duplicates by taking the mean if same date appears multiple times

combined_forecast_df = (

combined_forecast_df.groupby("date").mean().reset_index()

)

combined_forecast_df = combined_forecast_df.sort_values("date")

# Plot as a single continuous line

ax.plot(

combined_forecast_df["date"],

combined_forecast_df["forecast"],

color=COLORS[color_key],

linewidth=2,

alpha=0.7,

label=f"{label} (MAPE: {metrics['MAPE']:.2f}%)",

zorder=3,

)

# Add vertical line at the train/test split (where forecasts begin)

ax.axvline(

x=earliest_forecast_date,

color="red",

linestyle="--",

linewidth=2,

alpha=0.7,

label="Train/Test Split",

zorder=2,

)

# Set labels and title

ax.set_xlabel("Date")

ax.set_ylabel(f"{TARGET_COLUMN}")

ax.set_title("Forecast Comparison: All Scenarios")

# Add grid and legend

ax.grid(True, linestyle="--", alpha=0.3)

# Place legend inside plot area at lower left with 2 rows

ax.legend(loc="lower left", frameon=True, ncol=3)

# Format x-axis

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

# Save plot

plot_path = os.path.join(output_dir, "forecast_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Forecast comparison plot saved to: {plot_path}")

plt.close()

# Generate the plot

plot_forecast_comparison(df, responses, metrics_list)

Example Output: Forecast Comparison

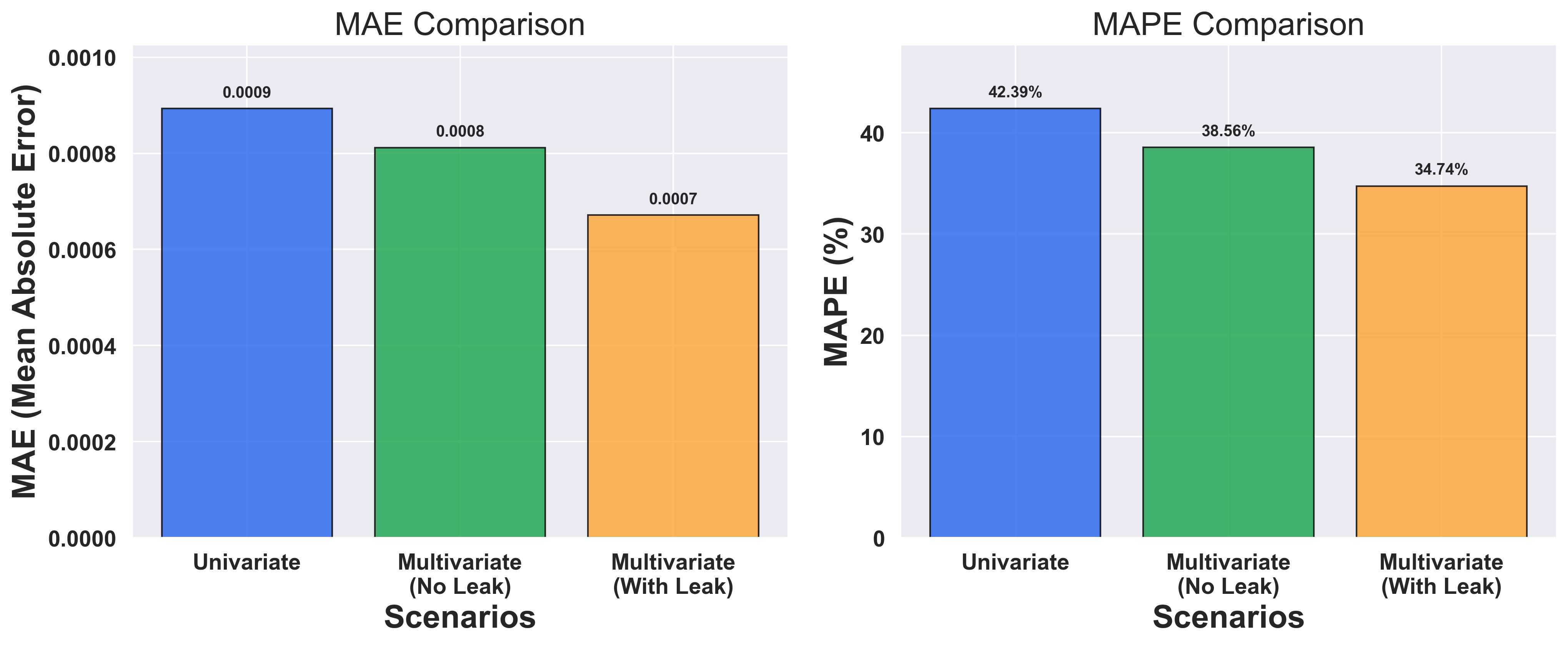

8. Metrics Comparison

Finally, let’s create a bar chart comparing the performance metrics:Show metrics comparison plotting code

Show metrics comparison plotting code

def plot_metrics_comparison(metrics_list, output_dir="usecases/economic_backtesting"):

"""

Plot bar chart comparing metrics across scenarios.

Args:

metrics_list: Tuple of (metrics1, metrics2, metrics3)

output_dir: Directory to save the plot

"""

os.makedirs(output_dir, exist_ok=True)

metrics1, metrics2, metrics3 = metrics_list

scenarios = [

"Univariate",

"Multivariate\n(No Leak)",

"Multivariate\n(With Leak)",

]

mae_values = [metrics1["MAE"], metrics2["MAE"], metrics3["MAE"]]

mape_values = [metrics1["MAPE"], metrics2["MAPE"], metrics3["MAPE"]]

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

x = np.arange(len(scenarios))

bar_colors = ["#2563eb", "#16a34a", "#fea333"]

# MAE plot

bars1 = ax1.bar(

x,

mae_values,

color=bar_colors,

alpha=0.8,

edgecolor="black",

linewidth=1,

)

for i, (bar, val) in enumerate(zip(bars1, mae_values)):

ax1.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mae_values) * 0.02,

f"{val:.4f}",

ha="center",

va="bottom",

fontsize=10,

)

ax1.set_xlabel("Scenarios")

ax1.set_ylabel("MAE (Mean Absolute Error)")

ax1.set_title("MAE Comparison")

ax1.set_xticks(x)

ax1.set_xticklabels(scenarios)

ax1.set_ylim(0, max(mae_values) * 1.15)

# MAPE plot

bars2 = ax2.bar(

x,

mape_values,

color=bar_colors,

alpha=0.8,

edgecolor="black",

linewidth=1,

)

for i, (bar, val) in enumerate(zip(bars2, mape_values)):

ax2.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mape_values) * 0.02,

f"{val:.2f}%",

ha="center",

va="bottom",

fontsize=10,

)

ax2.set_xlabel("Scenarios")

ax2.set_ylabel("MAPE (%)")

ax2.set_title("MAPE Comparison")

ax2.set_xticks(x)

ax2.set_xticklabels(scenarios)

ax2.set_ylim(0, max(mape_values) * 1.15)

plt.tight_layout()

# Save plot

plot_path = os.path.join(output_dir, "metrics_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Metrics comparison plot saved to: {plot_path}")

plt.close()

# Generate the plot

plot_metrics_comparison(metrics_list)

Example Output: Metrics Comparison

Key Insights

From this analysis, you can answer critical questions:- How much does context help? → Compare MAPE across scenarios to quantify improvement

- What If Forecasting Variables known in advance (like Fed Funds Rate) can be included as leak columns

Complete Code

Here’s the full working example you can run:Show complete code

Show complete code

import asyncio

import os

import matplotlib.pyplot as plt

import numpy as np

import pandas as pd

from fredapi import Fred

from haver import Haver

from sklearn.metrics import (

mean_absolute_error,

mean_absolute_percentage_error,

mean_squared_error,

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_unemployment_rate():

"""Retrieve Unemployment Rate from FRED."""

df = (

fred.get_series("UNRATE", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "UNRATE"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_consumer_price_index():

"""Retrieve Consumer Price Index from FRED."""

df = (

fred.get_series("CPIAUCSL", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "CPIAUCSL"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_sp500():

"""Retrieve S&P 500 Index from Haver."""

return get_haver_series("SP500@USECON", "SPY")

def create_combined_dataset():

"""Combine economic indicators into a single quarterly dataset."""

# Fetch all data sources

gdp_df = get_haver_gdp()

fed_funds = get_federal_funds_rate()

unemployment = get_unemployment_rate()

cpi = get_consumer_price_index()

sp500 = get_sp500()

# Merge monthly indicators

macro_df = (

fed_funds.merge(unemployment, on="date", how="outer")

.merge(cpi, on="date", how="outer")

.merge(sp500, on="date", how="outer")

)

macro_df["date"] = pd.to_datetime(macro_df["date"])

macro_df = macro_df.set_index("date")

# Join with GDP and forward-fill

gdp_df["date"] = pd.to_datetime(gdp_df["date"])

gdp_indexed = gdp_df.set_index("date")[["GDPH_pct_change"]]

combined_df = gdp_indexed.join(macro_df, how="outer")

combined_df["GDPH_pct_change"] = combined_df["GDPH_pct_change"].ffill()

# Calculate percent changes

for col in ["FEDFUNDS", "UNRATE", "CPIAUCSL", "SPY"]:

combined_df[f"{col}_pct_change"] = combined_df[col].pct_change()

# Filter and resample to quarterly

combined_df = combined_df[combined_df.index >= "1990-01-01"]

combined_df = combined_df.filter(like="_pct_change").ffill().dropna()

combined_df = combined_df.resample("QE").mean()

return combined_df

def plot_raw_time_series(df, output_dir="economic_backtesting"):

"""Plot raw time series data."""

os.makedirs(output_dir, exist_ok=True)

fig, ax = plt.subplots(figsize=(14, 6))

ax.plot(

df.index,

df[TARGET_COLUMN],

color=COLORS["groundtruth"],

linewidth=2,

label=f"{TARGET_COLUMN}",

zorder=2,

)

ax.set_xlabel("Date")

ax.set_ylabel(f"{TARGET_COLUMN}")

ax.set_title(f"Historical {TARGET_COLUMN} (1990-Present)")

ax.grid(True, linestyle="--", alpha=0.3)

ax.legend(loc="upper left", frameon=True)

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

plot_path = os.path.join(output_dir, "raw_time_series.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Raw time series plot saved to: {plot_path}")

plt.close()

def calculate_metrics(actual, predicted):

"""Calculate forecast accuracy metrics."""

mae = mean_absolute_error(actual, predicted)

rmse = np.sqrt(mean_squared_error(actual, predicted))

mape = mean_absolute_percentage_error(actual, predicted) * 100

return {"MAE": mae, "RMSE": rmse, "MAPE": mape}

def extract_actuals_and_predictions(response, request, df_with_date):

"""Extract actual and predicted values from forecast response."""

all_actuals = []

all_predictions = []

for forecast_row, sample in zip(response.forecasts, request.samples):

if forecast_row[0].values:

target_dates = pd.to_datetime(forecast_row[0].timestamps)

predictions = forecast_row[0].values

actuals = []

for date in target_dates:

actual_val = df_with_date[df_with_date["date"] == date][

TARGET_COLUMN

].values

if len(actual_val) > 0:

actuals.append(actual_val[0])

if len(actuals) == len(predictions):

all_actuals.extend(actuals)

all_predictions.extend(predictions)

return all_actuals, all_predictions

def plot_forecast_comparison(

df, responses, metrics_list, output_dir="economic_backtesting"

):

"""Plot comparison of all three forecasting scenarios."""

os.makedirs(output_dir, exist_ok=True)

response1, response2, response3 = responses

metrics1, metrics2, metrics3 = metrics_list

data_df = df.reset_index()[["date", TARGET_COLUMN]].copy()

# Find the earliest forecast date to determine train/test split

earliest_forecast_date = None

for forecast_row in response1.forecasts:

if forecast_row[0].values:

dates = pd.to_datetime(forecast_row[0].timestamps)

if earliest_forecast_date is None or dates.min() < earliest_forecast_date:

earliest_forecast_date = dates.min()

# Calculate cutoff to show last 50% of historical data before forecasts

historical_before_forecast = data_df[data_df["date"] < earliest_forecast_date]

cutoff_idx = int(len(historical_before_forecast) * 0.5)

cutoff_date = historical_before_forecast.iloc[cutoff_idx]["date"]

# Filter to show last 50% of historical data + all forecasts

data_df_filtered = data_df[data_df["date"] >= cutoff_date].copy()

fig, ax = plt.subplots(figsize=(14, 6))

# Plot ground truth

ax.plot(

data_df_filtered["date"],

data_df_filtered[TARGET_COLUMN],

color=COLORS["groundtruth"],

linewidth=2,

label="Actual",

zorder=4,

alpha=0.8,

)

# Plot forecasts for each scenario

scenarios = [

(response1, metrics1, "univariate", "Univariate"),

(response2, metrics2, "multivariate", "Multivariate (No Leak)"),

(response3, metrics3, "multivariate_leak", "Multivariate (With Leak)"),

]

FORECAST_WINDOW = 1 # Forecast 1 quarter ahead

NUM_BACKTEST_ROWS = 12 # Backtest last 12 quarters (3 years)

# Initialize Haver and FRED

haver = Haver(api_key=HAVER_API_KEY)

fred = Fred(api_key=FRED_API_KEY)

# Plot colors

COLORS = {

"univariate": "#2563eb",

"multivariate": "#16a34a",

"multivariate_leak": "#fea333",

"groundtruth": "black",

}

def get_haver_series(haver_code, column_name):

"""Retrieve data from Haver and calculate percent change."""

df = haver.read_df(haver_codes=[haver_code])

df = df[df.columns[df.columns.isin(["date", "value"])]]

df = df.dropna()

df = df.rename(columns={"value": column_name})

df["date"] = pd.to_datetime(df["date"])

pct_change_column = f"{column_name}_pct_change"

df[pct_change_column] = df[column_name].pct_change().dropna()

return df

def get_haver_gdp():

"""Retrieve Real GDP from Haver."""

return get_haver_series("GDPHA@USECON", "GDPH")

def get_federal_funds_rate():

"""Retrieve Federal Funds Effective Rate from FRED."""

df = (

fred.get_series("FEDFUNDS", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "FEDFUNDS"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_unemployment_rate():

"""Retrieve Unemployment Rate from FRED."""

df = (

fred.get_series("UNRATE", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "UNRATE"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_consumer_price_index():

"""Retrieve Consumer Price Index from FRED."""

df = (

fred.get_series("CPIAUCSL", observation_start="1990-01-01")

.reset_index()

.rename(columns={"index": "date", 0: "CPIAUCSL"})

)

df["date"] = pd.to_datetime(df["date"])

return df

def get_sp500():

"""Retrieve S&P 500 Index from Haver."""

return get_haver_series("SP500@USECON", "SPY")

def create_combined_dataset():

"""Combine economic indicators into a single quarterly dataset."""

# Fetch all data sources

gdp_df = get_haver_gdp()

fed_funds = get_federal_funds_rate()

unemployment = get_unemployment_rate()

cpi = get_consumer_price_index()

sp500 = get_sp500()

# Merge monthly indicators

macro_df = (

fed_funds.merge(unemployment, on="date", how="outer")

.merge(cpi, on="date", how="outer")

.merge(sp500, on="date", how="outer")

)

macro_df["date"] = pd.to_datetime(macro_df["date"])

macro_df = macro_df.set_index("date")

# Join with GDP and forward-fill

gdp_df["date"] = pd.to_datetime(gdp_df["date"])

gdp_indexed = gdp_df.set_index("date")[["GDPH_pct_change"]]

combined_df = gdp_indexed.join(macro_df, how="outer")

combined_df["GDPH_pct_change"] = combined_df["GDPH_pct_change"].ffill()

# Calculate percent changes

for col in ["FEDFUNDS", "UNRATE", "CPIAUCSL", "SPY"]:

combined_df[f"{col}_pct_change"] = combined_df[col].pct_change()

# Filter and resample to quarterly

combined_df = combined_df[combined_df.index >= "1990-01-01"]

combined_df = combined_df.filter(like="_pct_change").ffill().dropna()

combined_df = combined_df.resample("QE").mean()

return combined_df

def plot_raw_time_series(df, output_dir="economic_backtesting"):

"""Plot raw time series data."""

os.makedirs(output_dir, exist_ok=True)

fig, ax = plt.subplots(figsize=(14, 6))

ax.plot(

df.index,

df[TARGET_COLUMN],

color=COLORS["groundtruth"],

linewidth=2,

label=f"{TARGET_COLUMN}",

zorder=2,

)

ax.set_xlabel("Date")

ax.set_ylabel(f"{TARGET_COLUMN}")

ax.set_title(f"Historical {TARGET_COLUMN} (1990-Present)")

ax.grid(True, linestyle="--", alpha=0.3)

ax.legend(loc="upper left", frameon=True)

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

plot_path = os.path.join(output_dir, "raw_time_series.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Raw time series plot saved to: {plot_path}")

plt.close()

def calculate_metrics(actual, predicted):

"""Calculate forecast accuracy metrics."""

mae = mean_absolute_error(actual, predicted)

rmse = np.sqrt(mean_squared_error(actual, predicted))

mape = mean_absolute_percentage_error(actual, predicted) * 100

return {"MAE": mae, "RMSE": rmse, "MAPE": mape}

def extract_actuals_and_predictions(response, request, df_with_date):

"""Extract actual and predicted values from forecast response."""

all_actuals = []

all_predictions = []

for forecast_row, sample in zip(response.forecasts, request.samples):

if forecast_row[0].values:

target_dates = pd.to_datetime(forecast_row[0].timestamps)

predictions = forecast_row[0].values

all_forecast_dates.extend(dates)

all_forecast_values.extend(predictions)

if all_forecast_dates:

combined_forecast_df = pd.DataFrame(

{"date": all_forecast_dates, "forecast": all_forecast_values}

)

combined_forecast_df = (

combined_forecast_df.groupby("date").mean().reset_index()

)

combined_forecast_df = combined_forecast_df.sort_values("date")

ax.plot(

combined_forecast_df["date"],

combined_forecast_df["forecast"],

color=COLORS[color_key],

linewidth=2,

alpha=0.7,

label=f"{label} (MAPE: {metrics['MAPE']:.2f}%)",

zorder=3,

)

# Add vertical line at the train/test split

ax.axvline(

x=earliest_forecast_date,

color="red",

linestyle="--",

linewidth=2,

alpha=0.7,

label="Train/Test Split",

zorder=2,

)

ax.set_xlabel("Date")

ax.set_ylabel(f"{TARGET_COLUMN}")

ax.set_title("Forecast Comparison: All Scenarios")

ax.grid(True, linestyle="--", alpha=0.3)

ax.legend(loc="lower left", frameon=True, ncol=3)

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

plot_path = os.path.join(output_dir, "forecast_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Forecast comparison plot saved to: {plot_path}")

plt.close()

def plot_metrics_comparison(

metrics_list, output_dir="economic_backtesting"

):

"""Plot bar chart comparing metrics across scenarios."""

os.makedirs(output_dir, exist_ok=True)

metrics1, metrics2, metrics3 = metrics_list

scenarios = [

"Univariate",

"Multivariate\n(No Leak)",

"Multivariate\n(With Leak)",

]

mae_values = [metrics1["MAE"], metrics2["MAE"], metrics3["MAE"]]

mape_values = [metrics1["MAPE"], metrics2["MAPE"], metrics3["MAPE"]]

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

x = np.arange(len(scenarios))

bar_colors = [

COLORS["univariate"],

COLORS["multivariate"],

COLORS["multivariate_leak"],

]

# MAE plot

bars1 = ax1.bar(

x, mae_values, color=bar_colors, alpha=0.8, edgecolor="black", linewidth=1

)

for i, (bar, val) in enumerate(zip(bars1, mae_values)):

ax1.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mae_values) * 0.02,

f"{val:.4f}",

ha="center",

va="bottom",

fontsize=10,

)

ax1.set_xlabel("Scenarios")

ax1.set_ylabel("MAE (Mean Absolute Error)")

ax1.set_title("MAE Comparison")

ax1.set_xticks(x)

ax1.set_xticklabels(scenarios)

ax1.set_ylim(0, max(mae_values) * 1.15)

# MAPE plot

bars2 = ax2.bar(

x, mape_values, color=bar_colors, alpha=0.8, edgecolor="black", linewidth=1

)

for i, (bar, val) in enumerate(zip(bars2, mape_values)):

ax2.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mape_values) * 0.02,

f"{val:.2f}%",

ha="center",

va="bottom",

fontsize=10,

)

ax2.set_xlabel("Scenarios")

ax2.set_ylabel("MAPE (%)")

ax2.set_title("MAPE Comparison")

ax2.set_xticks(x)

ax2.set_xticklabels(scenarios)

ax2.set_ylim(0, max(mape_values) * 1.15)

plt.tight_layout()

plot_path = os.path.join(output_dir, "metrics_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Metrics comparison plot saved to: {plot_path}")

plt.close()

async def run_backtest(df, metadata_cols=None, leak_cols=None):

"""Generic backtesting function for target column forecasting."""

if metadata_cols is None:

data_df = df.reset_index()[["date", TARGET_COLUMN]].copy()

# Show only last 10% of data

total_rows = len(data_df)

cutoff_idx = int(total_rows * 0.9)

cutoff_date = data_df.iloc[cutoff_idx]["date"]

data_df_filtered = data_df[data_df["date"] >= cutoff_date].copy()

fig, ax = plt.subplots(figsize=(14, 6))

# Plot ground truth

ax.plot(

data_df_filtered["date"],

data_df_filtered[TARGET_COLUMN],

color=COLORS["groundtruth"],

linewidth=2,

label="Actual",

zorder=4,

alpha=0.8,

)

# Plot forecasts for each scenario

scenarios = [

(response1, metrics1, "univariate", "Univariate"),

(response2, metrics2, "multivariate", "Multivariate (No Leak)"),

(response3, metrics3, "multivariate_leak", "Multivariate (With Leak)"),

]

for response, metrics, color_key, label in scenarios:

all_forecast_dates = []

all_forecast_values = []

for forecast_row in response.forecasts:

if forecast_row[0].values:

dates = pd.to_datetime(forecast_row[0].timestamps)

predictions = forecast_row[0].values

all_forecast_dates.extend(dates)

all_forecast_values.extend(predictions)

if all_forecast_dates:

combined_forecast_df = pd.DataFrame(

{"date": all_forecast_dates, "forecast": all_forecast_values}

)

combined_forecast_df = (

combined_forecast_df.groupby("date").mean().reset_index()

)

combined_forecast_df = combined_forecast_df.sort_values("date")

ax.plot(

combined_forecast_df["date"],

combined_forecast_df["forecast"],

color=COLORS[color_key],

linewidth=2,

alpha=0.7,

label=f"{label} (MAPE: {metrics['MAPE']:.2f}%)",

zorder=3,

)

ax.set_xlabel("Date")

ax.set_ylabel(f"{TARGET_COLUMN}")

ax.set_title(

"Forecast Comparison: All Scenarios (Last 10% of History + Forecasts)"

)

ax.grid(True, linestyle="--", alpha=0.3)

ax.legend(loc="upper left", frameon=True)

plt.xticks(rotation=45, ha="right")

plt.tight_layout()

plot_path = os.path.join(output_dir, "forecast_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Forecast comparison plot saved to: {plot_path}")

plt.close()

def plot_metrics_comparison(

metrics_list, output_dir="economic_backtesting"

):

"""Plot bar chart comparing metrics across scenarios."""

os.makedirs(output_dir, exist_ok=True)

metrics1, metrics2, metrics3 = metrics_list

scenarios = [

"Univariate",

"Multivariate\n(No Leak)",

"Multivariate\n(With Leak)",

]

mae_values = [metrics1["MAE"], metrics2["MAE"], metrics3["MAE"]]

mape_values = [metrics1["MAPE"], metrics2["MAPE"], metrics3["MAPE"]]

fig, (ax1, ax2) = plt.subplots(1, 2, figsize=(14, 6))

x = np.arange(len(scenarios))

bar_colors = [

COLORS["univariate"],

COLORS["multivariate"],

COLORS["multivariate_leak"],

]

# MAE plot

bars1 = ax1.bar(

x, mae_values, color=bar_colors, alpha=0.8, edgecolor="black", linewidth=1

)

for i, (bar, val) in enumerate(zip(bars1, mae_values)):

ax1.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mae_values) * 0.02,

f"{val:.4f}",

ha="center",

va="bottom",

fontsize=10,

)

ax1.set_xlabel("Scenarios")

ax1.set_ylabel("MAE (Mean Absolute Error)")

ax1.set_title("MAE Comparison")

ax1.set_xticks(x)

ax1.set_xticklabels(scenarios)

ax1.set_ylim(0, max(mae_values) * 1.15)

# MAPE plot

bars2 = ax2.bar(

x, mape_values, color=bar_colors, alpha=0.8, edgecolor="black", linewidth=1

)

for i, (bar, val) in enumerate(zip(bars2, mape_values)):

ax2.text(

bar.get_x() + bar.get_width() / 2,

bar.get_height() + max(mape_values) * 0.02,

f"{val:.2f}%",

ha="center",

va="bottom",

fontsize=10,

)

ax2.set_xlabel("Scenarios")

ax2.set_ylabel("MAPE (%)")

ax2.set_title("MAPE Comparison")

ax2.set_xticks(x)

ax2.set_xticklabels(scenarios)

ax2.set_ylim(0, max(mape_values) * 1.15)

plt.tight_layout()

plot_path = os.path.join(output_dir, "metrics_comparison.png")

plt.savefig(plot_path, dpi=300, bbox_inches="tight")

print(f"Metrics comparison plot saved to: {plot_path}")

plt.close()

async def run_backtest(df, metadata_cols=None, leak_cols=None):

"""Generic backtesting function for target column forecasting."""

if metadata_cols is None:

data_df = df.reset_index()[["date", TARGET_COLUMN]].copy()

metadata_cols = []

else:

data_df = df.reset_index().copy()

request = ForecastV2Request.from_dfs_pre_split(

dfs=[data_df],

timestamp_col="date",

target_cols=[TARGET_COLUMN],

model="Migas-1.0",

num_target_rows=NUM_BACKTEST_ROWS,

forecast_window=FORECAST_WINDOW,

stride=FORECAST_WINDOW,

metadata_cols=metadata_cols,

leak_cols=leak_cols or [],

)

async with SynthefyAsyncAPIClient() as client:

response = await client.forecast(request)

all_actuals, all_predictions = extract_actuals_and_predictions(

response, request, data_df

)

metrics = calculate_metrics(all_actuals, all_predictions)

return metrics, response

def print_comparison_summary(metrics1, metrics2, metrics3):

"""Print formatted comparison table."""

print(f"\n{'Scenario':<45} {'MAE':>10} {'RMSE':>10} {'MAPE':>10}")

print("-" * 80)

scenarios = [

("1. Univariate (target only)", metrics1),

("2. Multivariate (No Leak)", metrics2),

("3. Multivariate (With Leak)", metrics3),

]

for name, m in scenarios:

print(

f"{name:<45} {m['MAE']:>10.6f} {m['RMSE']:>10.6f} {m['MAPE']:>9.2f}%"

)

async def run_all_backtests():

"""Run all three backtesting scenarios and compare results."""

df = create_combined_dataset()

plot_raw_time_series(df)

results = await asyncio.gather(

run_backtest(df, metadata_cols=None, leak_cols=None),

run_backtest(df, metadata_cols=METADATA_COLUMNS, leak_cols=None),

run_backtest(

df, metadata_cols=METADATA_COLUMNS, leak_cols=METADATA_COLUMNS

),

)

metrics1, response1 = results[0]

metrics2, response2 = results[1]

metrics3, response3 = results[2]

print_comparison_summary(metrics1, metrics2, metrics3)

plot_forecast_comparison(

df,

(response1, response2, response3),

(metrics1, metrics2, metrics3),

)

plot_metrics_comparison((metrics1, metrics2, metrics3))

def main():

"""Main function to run backtesting analysis."""

return asyncio.run(run_all_backtests())

if __name__ == "__main__":

results = main()

Next Steps

- Try different target variables: Forecast unemployment, S&P 500, or other economic indicators

- Adjust forecast horizon: Change

NUM_BACKTEST_ROWSto change the backtesting period - Add more economic data: Include additional indicators from FRED or Haver, or your own